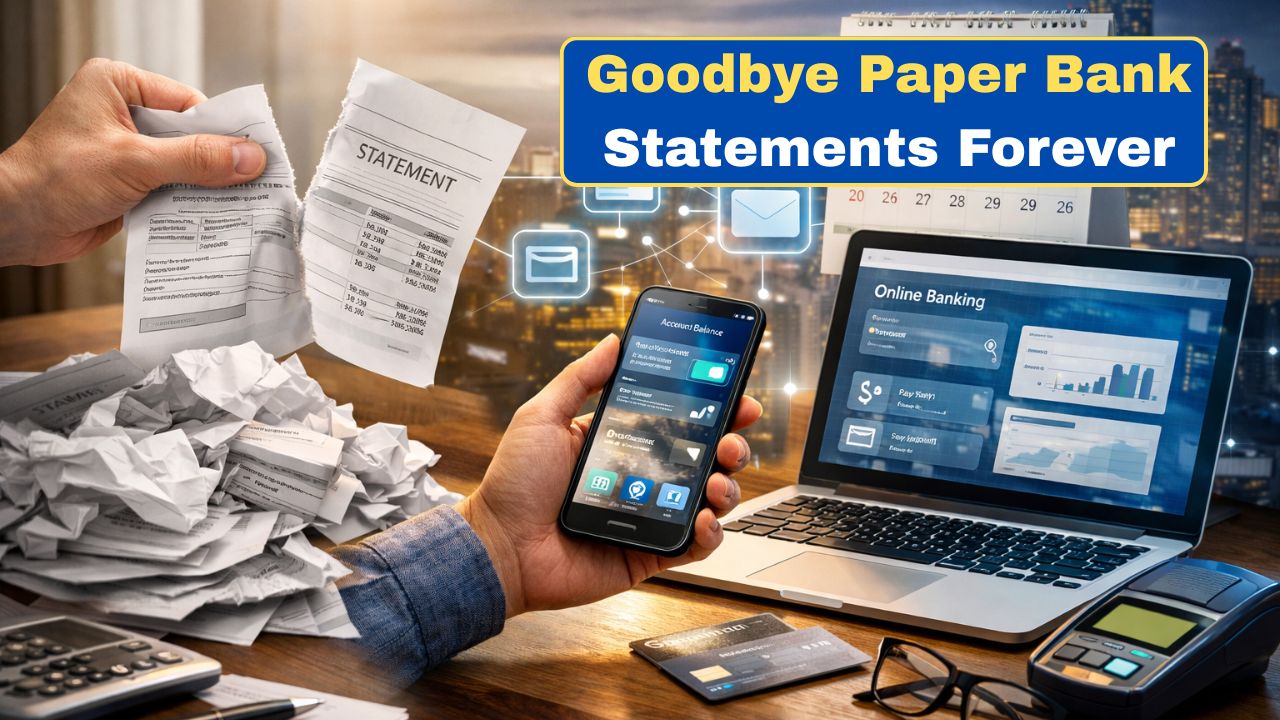

Starting February 2026, banks across the United States will implement a major shift by phasing out traditional paper statements in favor of fully digital communications. This move is part of a broader trend toward automation, cost efficiency, and environmental responsibility. Along with this transition, a new set of digital fee rules will come into effect, impacting how customers are charged for various account services. Many consumers will need to update their preferences and understand new fees associated with non-digital banking options. This change underscores the increasing need for digital banking awareness, online account access, and secure communication preferences.

Paperless Banking Becomes the Norm

As more banks embrace sustainability and cost reduction, the traditional paper statement is on its way out. In February 2026, most U.S. banks will default to digital-only statements, unless customers specifically opt out. This shift reduces the environmental impact of paper printing waste and cuts down on mailing costs for institutions. However, those who still prefer printed statements may now face monthly paper fees. Consumers are urged to ensure their email addresses are updated to receive timely statements and alerts.

New Digital Fee Structures Introduced

Alongside the paperless switch, banks will introduce new digital fee rules starting February 2026. These include charges for in-person service requests that could be done online, or for paper-based statement requests. The new system is designed to reward online self-service users while encouraging a move away from legacy banking methods. Customers who regularly rely on physical mail updates or branch visits may see an uptick in fees unless they transition to mobile or web platforms.

How Consumers Can Prepare

To avoid unnecessary charges, consumers should act before the February 2026 rollout. It’s critical to log into your bank’s website and review your communication preferences. Activating email or app notifications will ensure that monthly statements arrive digitally. Many banks are offering incentives such as fee waivers or bonus rewards for early adoption. Those unsure about navigating digital platforms should reach out to their bank’s online support team for guidance and setup help.

Summary: Digital Shift With Real Impact

The phase-out of paper statements marks a major evolution in consumer banking across the U.S. While the environmental and cost-saving benefits are clear, the introduction of new digital fee structures means some customers may face higher charges if they don’t adapt. This is a pivotal moment for both older and tech-cautious users to become more digitally engaged with their banks. Planning ahead, updating your account settings, and seeking support can make this transition smooth and even financially beneficial.

| Change | Details |

|---|---|

| Paper Statement Default | Switched to digital-only |

| Effective Date | February 2026 |

| Paper Statement Fee | $2–$5 per month |

| Digital Incentives | Fee waivers, cashback offers |

| Action Required | Update preferences online |

| Support Available | Phone, email, chat support |

Frequently Asked Questions (FAQs)

1. When does the paperless transition begin?

Most U.S. banks will start on February 1, 2026.

2. Can I still get paper statements?

Yes, but you may have to pay a monthly fee.

3. How do I avoid new digital fees?

Switch to online statements and self-service banking.

4. What if I need help going digital?

Banks are offering phone and in-branch tech support.

Leave a Reply